Every Little Thing You Need To Understand About House Mortgages

Article by-Svenningsen SalomonsenIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

Organize your financial life before going after a home mortgage. If your paperwork is all over the place and confusing, then you'll just make the entire mortgage process that much longer. Do yourself and your lender a favor and put your financial papers in order prior to making any appointments.

Do not sign up with the first mortgage lender that you come across. There are so many out there that you would be doing yourself a disservice by being hasty. You should shop around a bit to make sure that the rate you are being offered is fair and competitive.

If https://www.cnbc.com/2021/05/03/irelands-banking-landscape-is-undergoing-drastic-change.html are a veteran of the U.S. Armed Forces, you may qualify for a VA morgtage loan. These loans are available to qualified veterens. The advantage of these loans is an easier approval process and a lower than average interest rate. The application process for these loans is not often complicated.

If the idea of a mortgage looming over your head for the next few decades does not appeal to you, consider refinancing over a shorter period. Although your monthly payments will be more, you'll save a lot in terms of interest over the life of the loan. It also means being mortgage-free much sooner, and owning your home outright!

Before starting the loan process, get all your documents together. All lenders will require certain documents. These documents include prior year tax returns, bank statements, and recent pay stubs. Being organized will help visit the up coming internet page along smoother.

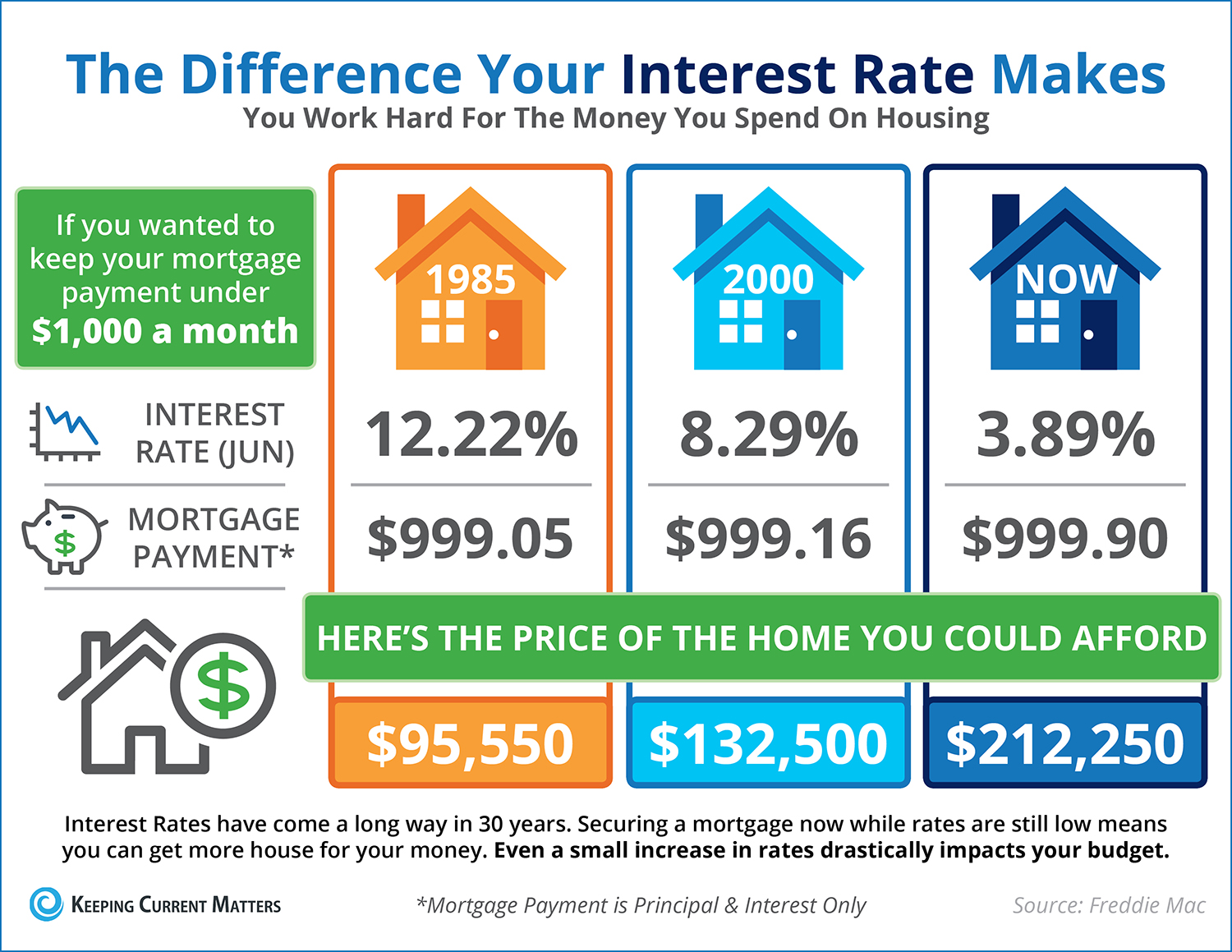

Check out the interest rates for 15, 20 and 30 year term lengths. Many times the shorter the term length the lower the interest rate. Although you may think you payment will be higher on a shorter term loan, you can actually save money on your payment by choosing a lower interest rate and a shorter term.

A good credit score is essential if you want to finance a home. If your score is below 600 you have some work to do before you can hope to purchase a home. Begin by getting a copy of your credit record and verifying that all the information on it is correct.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Make certain you check out many different financial institutions before you choose which one you will use as your mortgage lender. Check for reviews online and from your friends, and find information about their rates and hidden fees. You will be better able to pick the mortgage that is right for you when you have the details of each offer.

Find out how much your mortgage broker will be making off of the transaction. Many times mortgage broker commissions are negotiable just like real estate agent commissions are negotiable. Get this information and writing and take the time to look over the fee schedule to ensure the items listed are correct.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

If you are thinking abut changing jobs, try to wait until after your loan approval process is over. This is because the underwriter will have to go through the employment verification process all over again. They will also require you to submit paycheck information, which means that you would have to put the loan off until after you are paid a few times.

Never assume that a good faith estimate is fact or written in stone. It is in fact not just an estimate, but one written in good faith. Always be wary of extra costs and fees that can creep into the official and formal paperwork later that drive up your total expense.

Never assume that a mortgage is going to just get a home for you outright. Most lenders are going to require you to chip in a down payment. Depending on the lender, this can be anywhere from 5 percent to a full fifth of the total home value. Make sure you have this saved up.

Be sure to gather all your financial documentation and have it ready in a single file before applying for a home mortgage. You will need to have bank statements, tax returns, W2 forms and pay stubs on hand. Some lenders require additional documentation of income and responsibility. Be sure to find out what is needed before applying.

Understand what happens if you stop paying your home mortgage. It's important to get what the ramifications are so that you really know the seriousness of such a big loan as a home mortgage. Not paying can lead to a lower credit score and potentially losing your home! It's a big deal.

Most financial institutions want the assurance that the property they finance is insured and the property taxes are current. They do this by requiring that you add an amount to cover those expenses to your mortgage payments. This is called an escrow account, and most people find it is convenient to set up payments this way.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

With these tips, you'll be sure to find exactly the mortgage you need for your home. From buying new to refinancing your current home, the lenders are just waiting for your call. Get in touch now to see what you can do to pay for your home without breaking the bank.