Usual Solution To Home Mortgage Questions

Content create by-Pittman SlaughterIf you're looking into home mortgages, then you surely are excited. It's time to buy a home! However, what you might realize is there is quite a lot of information to take in, and how do you sort all of this out to get to the mortgage company and product that you need? Keep reading to find out how to do this.

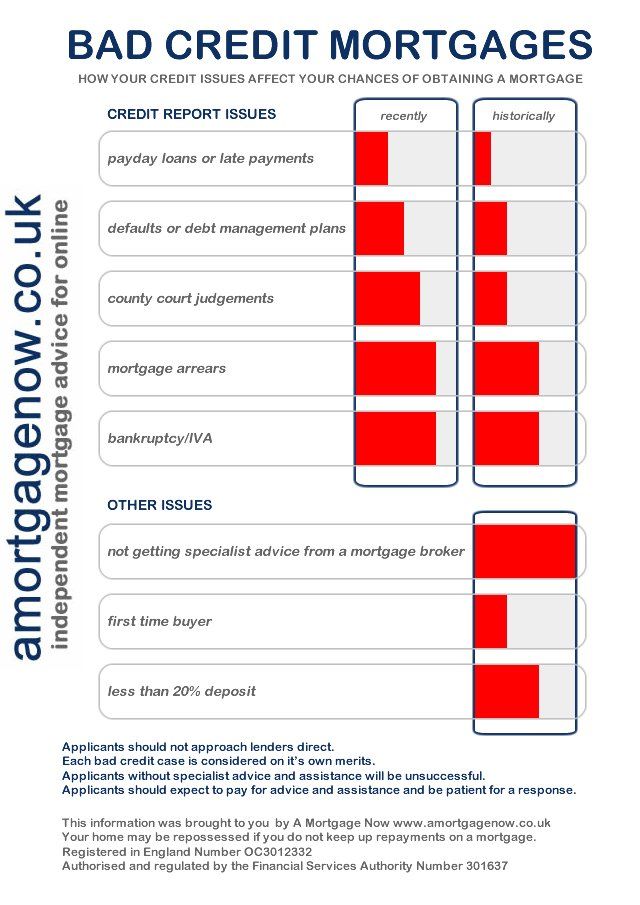

Before trying to get a mortgage approval, find out your credit score. Mortgage lenders can deny a loan when the borrower has a low credit score caused by late payments and other negative credit history. If your credit score is too low to qualify for a mortgage loan, clean up your credit, fix any inaccuracies and make all your payments on time.

Reduce or get rid of your debt before starting to apply for mortgage loans. When you apply for a home loan, lenders will look at how much debt you're carrying. If you have very little, you could be given a better loan for more money. High consumer debt could lead to a denial of your mortgage loan application. More debt can also lead to an increase in your mortgage rate, which you would rather avoid.

Knowing your credit score is important before trying to obtain a mortgage. The better your credit history and score, the easier it will be for you to get a mortgage. Examine visit this website link for any errors that might be unnecessarily lowering your score. In reality, to obtain a mortgage, your credit score should be 620 or higher.

Have the necessary documents ready. There are a few documents that you'll be expected to have when you come in for a home mortgage. You'll need to provide bank statements, income tax reports, W-2 statements, and at least two pay stubs. Having these at the ready will help make your meetings go much quicker.

Hire an attorney to help you understand your mortgage terms. Even those with degrees in accounting can find it difficult to fully understand the terms of a mortgage loan, and just trusting someone's word on what everything means can cause you problems down the line. Get an attorney to look it over and make everything clear.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Make sure you're not looking at any penalties when you apply for a new mortgage. Your old mortgage may impose fines for early payment, which can include refinancing. If there are fines, weigh the pros and cons before getting into a new mortgage, as you may end up paying a lot more than you expected, even though refinancing means a lower monthly payment.

When trying to figure out how much of a mortgage payment you can afford every month, do not neglect to factor in all the other costs of owning a home. There will be homeowner's insurance to consider, as well as neighborhood association fees. If you have previously rented, you might also be new to covering landscaping and yard care, as well as maintenance costs.

Know the real estate agency or home builder you are dealing with. It is common for builders and agencies to have their own in-house financiers. Ask the about their lenders. Find out their available loan terms. This could open a new avenue of financing up for your new home mortgage.

Pay your credit cards on time if you are considering a home mortgage in the next few years. Your credit score and debt to income ratios will come into play when you go for a home mortgage. If you have multiple late payments or are carrying a lot of debt, you may find the mortgage offers you receive to be poor.

Avoid a home mortgage that has a variable interest rate. If the economy changes, your rates can go through the roof. This could result in you no longer being able to afford your home, which you, of course, do not want to see happen.

If you are thinking abut changing jobs, try to wait until after your loan approval process is over. This is because the underwriter will have to go through the employment verification process all over again. They will also require you to submit paycheck information, which means that you would have to put the loan off until after you are paid a few times.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

During your application for a home loan, get a rate-lock. A rate-lock in writing guarantees certain terms and interest rates for a given period of time. Set the rate-lock "on application" instead of "on approval". The lock-in period needs to be long enough to allow for factors that can delay the loan process.

When the lending market is tight, having a good credit score is vital to securing a favorable mortgage rate. Get your credit reports from the big three agencies to make sure they contain no errors. Banks typically don't approve anyone with a score of less than 620 today.

Before applying for a home mortgage, get your debts in order. Consolidate small debts with high interest rates and put a solid effort into paying them off. Do not take on new debt while you are preparing to apply for a home mortgage. The cleaner your debt record when you apply for a home mortgage, the better your chances of getting approval for a good loan at a good rate.

Investigate preapprovals before you start home shopping. Preapproved mortgages will give you an idea of both how much home you can afford plus what your monthly mortgage payments will be. This will set the parameters of your home shopping and save you time not looking at properties you can't realistically afford.

When the bank asks a question, be honest. It is a terrible idea to lie when applying for mortgage loans. Never misstate assets or income. If you do you could find yourself saddled with more debt than you can actually afford to pay. It may seem good in the moment, but in the long-run it will haunt you.

There are a world of many mortgage companies out there vying for your business. It is you that has the power for any of them to put you in the right mortgage vehicle. So, don't let yourself be persuaded into something you don't want; instead, find a mortgage that fits your needs today.